CoreLogic’s latest Home Price Index reports that home prices have appreciated by 7.0% over the last 12 months. The same report predicts that prices will continue to increase at a rate of 5.2% over the next year.

The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

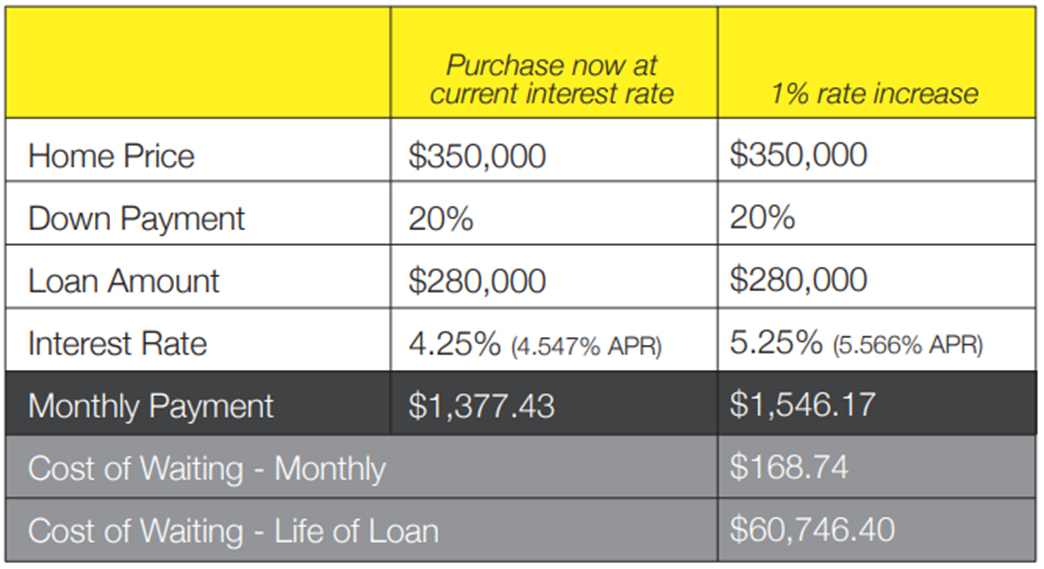

Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage have already increased by half of a percentage point, to around 4.5%, in 2018. Most experts predict that rates will rise over the next 12 months. The Mortgage Bankers Association, Fannie Mae, Freddie Mac, and the National Association of Realtors are in unison, projecting that rates will increase by half a percentage point by this time next year.

An increase in rates will impact YOUR monthly mortgage payment. A year from now, your housing expense will increase if a mortgage is necessary to buy your next home.

There are some renters who have not yet purchased a home because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that unless you are living with your parents rent-free, you are paying a mortgage - either yours or your landlord’s.

As an owner, your mortgage payment is a form of ‘forced savings’ that allows you to have equity in your home that you can tap into later in life. As a renter, you guarantee your landlord is the person with that equity.

Are you ready to put your housing cost to work for you?

The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears that both are on the rise.

But what if they weren’t? Would you wait?

Look at the actual reason you are buying and decide if it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer, or you just want to have control over renovations, maybe now is the time to buy.

| % of Buyers | Median Age | ||

|---|---|---|---|

|

All First-Time Homebuyers |

100% | 32 |

|

Married Couples |

57% | 32 |

|

Single

Females |

18% | 35 |

|

Unmarried

Couples |

16% | 30 |

|

Single

Males |

7% | 31 |

In this day and age of being able to shop for anything anywhere, it is really important to know what you’re looking for when you start your home search.

If you’ve been thinking about buying a home of your own for some time now, you’ve probably come up with a list of things that you’d LOVE to have in your new home. Many new homebuyers fantasize about the amenities that they see on television or Pinterest, and start looking at the countless homes listed for sale with rose-colored glasses.

Do you really need that farmhouse sink in the kitchen in order to be happy with your home choice? Would a two-car garage be a convenience or a necessity? Could the man cave of your dreams be a future renovation project instead of a make or break now?

The first step in your home buying process should be to get pre-approved for your mortgage. This allows you to know your budget before you fall in love with a home that is way outside of it.

The next step is to list all the features of a home that you would like, and to qualify them as follows:

‘Must-Haves’ – if this property does not have these items, then it shouldn’t even be considered. (ex: distance from work or family, number of bedrooms/bathrooms)

‘Should-Haves’ – if the property hits all of the 'must-haves' and some of the 'should- haves,' it stays in contention, but does not need to have all of these features.

‘Absolute-Wish List’ – if we find a property in our budget that has all of the ‘must-haves,’ most of the ‘should-haves,’ and ANY of these, it’s the winner!

Having this list fleshed out before starting your search will save you time and frustration, while also letting your agent know what features are most important to you before he or she begins to show you houses in your desired area.

There are many misconceptions about buying a home that are believed to be true. Let’s take a look at two of the more common ones that may be holding you back from buying today.

Buyers often overestimate the down payment funds needed to qualify for a home loan. Freddie Mac recently published an article entitled, “Debunking the 20% Down Myth,” which revealed that “the average down payment for first-time homebuyers in 2017 was 5%, and 10% for repeat buyers.”

While many believe that they need at least 20% down to buy their dream homes, they do not realize that there are programs available which allow them to put down as little as 3%. Many renters may actually be able to enter the housing market sooner than they had ever imagined with programs that have emerged allowing less cash out of pocket.

According to the same article:

“Many potential buyers are unaware of the fact that their down payment can come from sources other than personal savings. Some mortgage products let you use gifts from your family or employer. Others let you use grants or loans from non-for-profit or government agencies.”

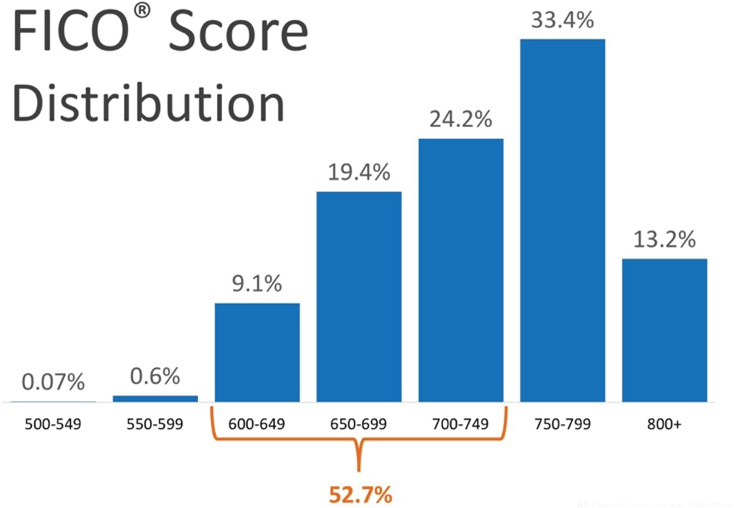

Similar to the down payment, many either don’t know or are misinformed about what FICO® score is necessary to qualify for a home loan.

Many Americans believe that a ‘good’ credit score is 780 or higher.

To help debunk this myth, let’s take a look at Ellie Mae’s latest Origination Insight Report which focuses on recently closed (approved) loans.

As you can see on the right, 52.7% of approved mortgages had a credit score of 600-749.

Whether buying your first home or moving up to your dream home, knowing your options will make the mortgage process easier. Your dream home may already be within your reach.

The American Dream of homeownership is alive and well. Recent reports show that the U.S. homeownership rate has rebounded from previous lows and is headed in the right direction. The personal reasons to own differ for each buyer, but there are many basic similarities.

Today we want to talk about the top 5 financial reasons you should own your own home.

Paying your mortgage each month allows you to build equity in your home that you can tap into later in life for renovations, to pay off high-interest credit card debt, or even send a child to college. As a renter, you guarantee that your landlord is the person with that equity.

One way to save on taxes is to own your own home. You may be able to deduct your mortgage interest, property taxes, and profits from selling your home, but make sure to always check with your accountant first to find out which tax advantages apply to you in your area.

When you purchase your home with a fixed-rate mortgage, you lock in your monthly housing cost for the next 5, 15, or 30 years. Interest rates remained around 4% all last year,marking some of the lowest rates in history. The value of your home will continue to rise with inflation, but your monthly costs will not.

The results of the 2018 Rental Affordability Report from ATTOM show that buying a median- priced home is more affordable than renting a three-bedroom property in 54% of U.S. counties analyzed for the report.

You can choose to invest your money in gold or the stock market, but you will still need somewhere to live. In a home that you own, you can wake up every morning knowing that your investment is gaining value while providing you a safe place to live.

Before you sign another lease, let’s get together to help you better understand all your options.

In many markets across the country, the number of buyers searching for their dream homes greatly exceeds the number of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search.

Even if you are in a market that is not as competitive, knowing your budget will give you the confidence to know if your dream home is within your reach.

Freddie Mac lays out the advantages of pre-approval in the 'My Home' section of their website.

“It’s highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you how much home you can afford and can help you move faster, and with greater confidence, in competitive markets.”

One of the many advantages of working with a local real estate professional is that many have relationships with lenders who will be able to help you with this process. Once you have selected a lender, you will need to fill out their loan application and provide them with important information regarding “your credit, debt, work history, down payment and residential history.”

Freddie Mac describes the '4 Cs' that help determine the amount you will be qualified to borrow:

1.Capacity: Your current and future ability to make your payments

2.Capital or Cash Reserves: The money, savings, and investments you have that can be sold quickly for cash

3.Collateral: The home, or type of home, that you would like to purchase

4.Credit: Your history of paying bills and other debts on time

Getting pre-approved is one of many steps that will show home sellers that you are serious about buying, and it often helps speed up the process once your offer has been accepted

Many potential homebuyers overestimate the down payment and credit scores needed to qualify for a mortgage today. If you are ready and willing to buy, you may be surprised at your ability to do so.

If you’ve entered the real estate market, as a buyer or a seller, you’ve inevitably heard the real estate mantra, “location, location, location” in reference to how identical homes can increase or decrease in value due to where they’re located. Well, a recent survey shows that when it comes to choosing a real estate agent, the millennial generation’s mantra is, “local, local, local.”

CentSai, a financial wellness online community, surveyed over 2,000 millennials (ages 18-34) and found that 75% of respondents would use a local real estate agent over an online agent, and 71% would choose a local lender.

Survey respondents cited many reasons for their choice to go local, “including personal touch & hand holding, long standing relationships, local knowledge, and amount of hassle.”

Doria Lavagnino, Cofounder & President of CentSai, had this to say:

“We were surprised to learn that online providers are not yet as big a disrupter in this sector as we first thought, despite purported cost savings. We found that millennials place a high value on the personal touch and knowledge of a local agent. Buying a home for the first time is daunting, and working with a local agent—particularly an agent referred by a parent or friend—could provide peace of mind.”

The findings of the CentSai survey are consistent with the Consumer Housing Trends Study, which found that millennials prefer a more hands-on approach to their real estate experience:

“While older generations rely on real estate agents for information and expertise, Millennials expect real estate agents to become trusted advisers and strategic partners.”

When it comes to choosing an agent, millennials and other generations share their top priority: the sense that an agent is trustworthy and responsive to their needs.

That said, technology still plays a huge role in the real estate process. According to the National Association of Realtors, 94% of home buyers look for prospective homes and neighborhoods online, and 74% also said they would use an online site or mobile app to research homes they might consider purchasing.

Many wondered if this tech-savvy generation would prefer to work with an online agent or lender, but more and more studies show that when it comes to real estate, millennials want someone they can trust, someone who knows the neighborhood they want to move into, leading them through the entire experience.

There are many potential homebuyers, and even sellers, who believe that you need at least a 20% down payment in order to buy a home or move on to their next home. Time after time, we have dispelled this myth by showing that there are many loan programs that allow you to put down as little as 3% (or 0% with a VA loan).

If you have saved up your down payment and are ready to start your home search, one other piece of the puzzle is to make sure that you have saved enough for your closing costs.

Freddie Mac defines closing costs as follows:

“Closing costs, also called settlement fees, will need to be paid when you obtain a mortgage. These are fees charged by people representing your purchase, including your lender, real estate agent, and other third parties involved in the transaction.

Closing costs are typically between 2 & 5% of your purchase price.”

We’ve recently heard from many first-time homebuyers that they wished that someone had let them know that closing costs could be so high. If you think about it, with a low down payment program, your closing costs could equal the amount that you saved for your down payment.

Here is a list of just some of the fees/costs that may be included in your closing costs, depending on where the home you wish to purchase is located:

Work with your lender and real estate agent to see if there are any ways to decrease or to include your closing costs into the mortgage as a Seller Concession. Homebuyers can also negotiate with the seller over who pays these fees. Sometimes the seller will agree to assume the buyer’s closing fees in order to get the deal finalized.

Speak with your lender and agent early and often to determine how much you’ll be responsible for at closing. Finding out you’ll need to come up with thousands of dollars right before closing is not a surprise anyone is ever looking forward to.

So you’ve been searching for that perfect house to call 'home' and you've finally found it! The price is right and, in such a competitive market, you want to make sure you make a good offer so that you can guarantee that your dream of making this house yours comes true!

Below are 4 steps provided by Freddie Mac to help buyers make offers, along with some additional information for your consideration:

“You’ve found the perfect home and you’re ready to buy. Now what? Your real estate agent will be by your side, helping you determine an offer price that is fair.”

Based on your agent’s experience and key considerations (like similar homes recently sold in the same neighborhood or the condition of the house and what you can afford), your agent will help you to determine the offer that you are going to present.

Getting pre-approved will not only show home-sellers that you are serious about buying, but it will also allow you to make your offer with confidence because you’ll know that you have already been approved for a mortgage in that amount.

“Once you’ve determined your price, your agent will draw up an offer, or purchase agreement, to submit to the seller’s real estate agent. This offer will include the purchase price and terms and conditions of the purchase.”

Talk with your Weichert agent to find out if there are any ways in which you can make your offer stand out in this competitive market! A licensed real estate agent who is active in the neighborhoods you are considering will be instrumental in helping you put in a solid offer.

“Oftentimes, the seller will counter the offer, typically asking for a higher purchase price or to adjust the closing date. In these cases, the seller’s agent will submit a counteroffer to your agent, detailing their desired changes, at this time, you can either accept the offer or decide if you want to counter.

Each time changes are made through a counteroffer, you or the seller have the option to accept, reject or counter it again. The contract is considered final when both parties sign the written offer.”

If your offer is approved, Freddie Mac urges you to “always get an independent home inspection, so you know the true condition of the home.” If the inspector uncovers undisclosed problems or issues, you can discuss any repairs that may need to be made with the seller or even cancel the contract altogether.

The inventory of homes listed for sale has remained well below the 6-month supply that is needed for a ‘normal’ market. Buyer demand has continued to outpace the supply of homes for sale, causing buyers to compete with each other for their dream homes.

Make sure that as soon as you decide that you want to make an offer, you work with your agent to present it as quickly as possible.

Whether buying your first home or your fifth, having a local real estate professional who is an expert in his or her market on your side is your best bet in making sure the process goes smoothly. Let’s talk about how we can make your dream of homeownership a reality!